.avif)

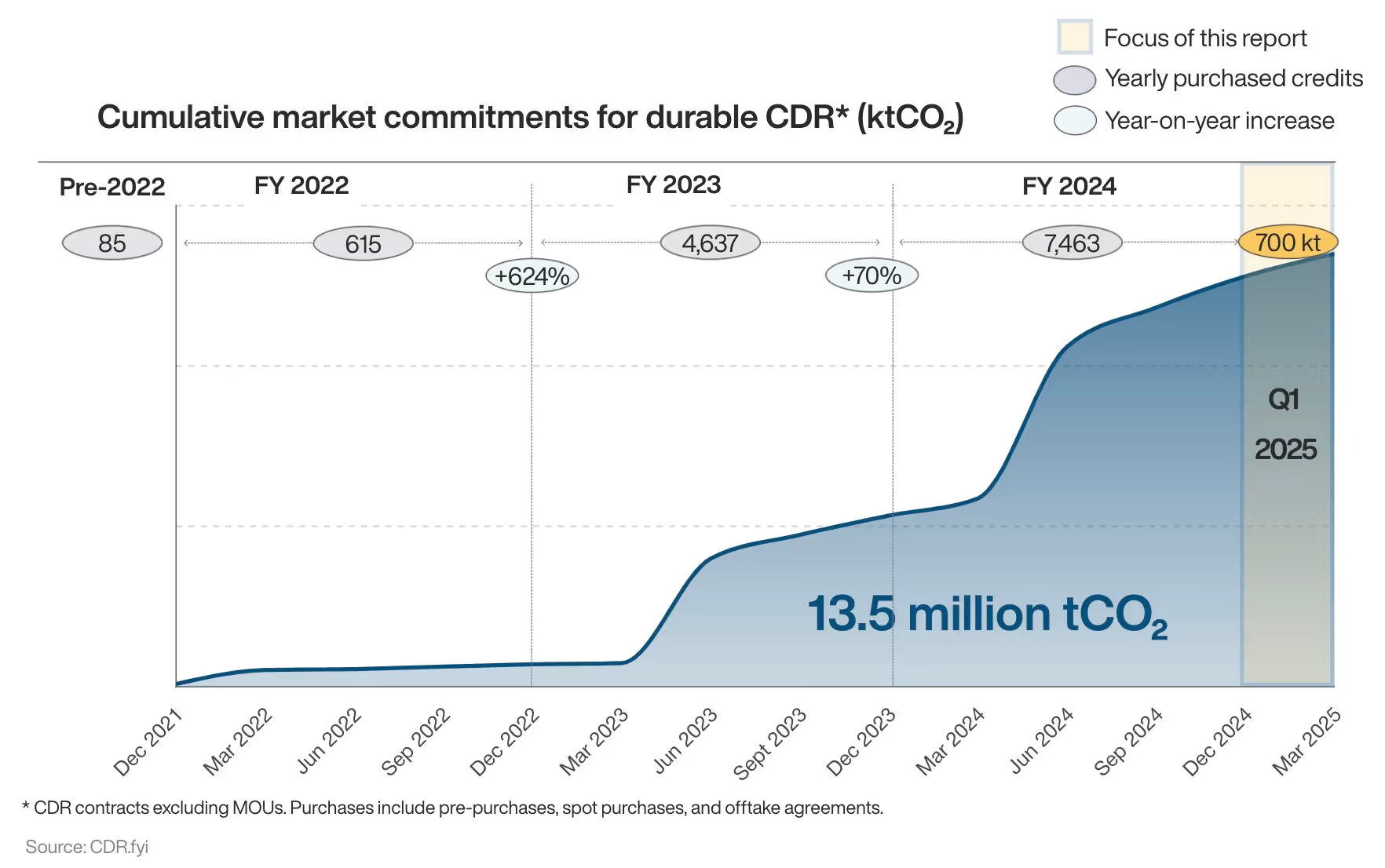

In Q1 this year, the durable CDR market recorded steady growth: 700 kilo-tonnes (kt) of new CDR contracts were signed, marking a 32% increase vs Q1 2024. This represents the highest ever amount of durable CDR purchased in the first quarter of a year.

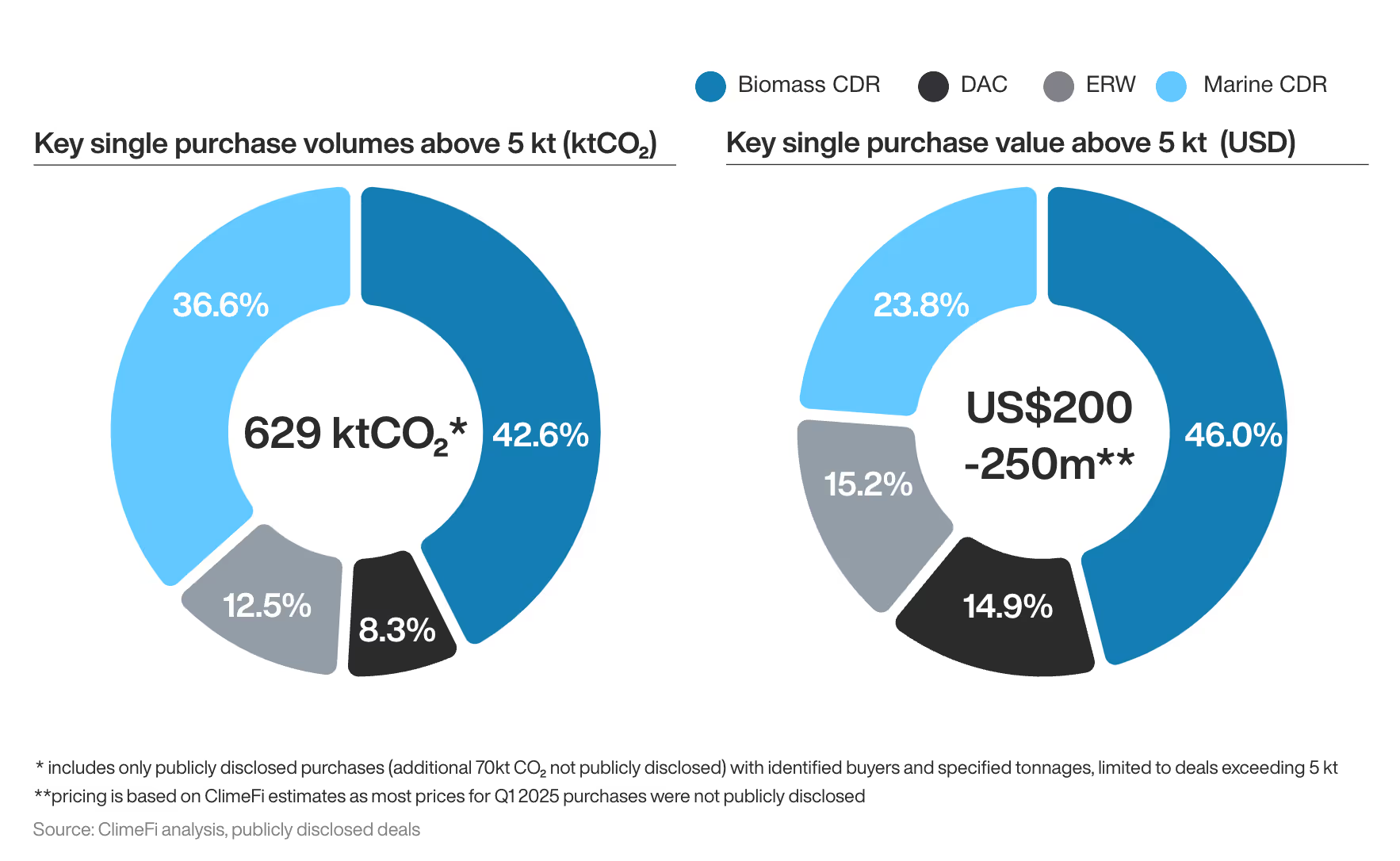

As of 31st March, cumulative market commitments for durable CDR amounted to more than 13.5 million tonnes. In terms of pathways, Biomass CDR led the way in Q1 with 260 kt of CDR credits purchased, accounting for 42.6% of total volume. Reflecting the increased interest in the pathway in recent months, Marine CDR followed closely behind with 36% of the market share and 230 kt credits purchased – the highest ever amount of Marine CDR purchased in a single quarter.

Google buys big, SkiesFifty breaks new ground

Along with some familiar names, Q1 also saw exciting new entrants to the CDR market. Deals were spread across a wide variety of pathways, including Marine CDR, Biochar, Bio-oil, Direct Air Capture (DAC), and Enhanced Rock Weathering (ERW).

In January, Google signed the largest Biochar-based removal agreement to date, purchasing 100 ktCO₂ of Biochar from Varaha and 100 ktCO₂ of Bio-oil from Charm Industrial. This is the third quarter in a row that Google has purchased more than 100 ktCO₂, further cementing its position as one of the leading players in the durable CDR market.

Another significant deal lies with SkiesFifty – an investment company dedicated to sustainable aviation – who signed an agreement with Gigablue for 200kt of Marine CDR over the next four years. This was the largest Marine CDR deal ever, and could pave the way for future transactions in a rapidly growing space. Together, Google and SkiesFifty accounted for 64% of all purchases in Q1.

For the fourth quarter in a row, Frontier purchased CDR – this time on two separate occasions, securing a cumulative total of 125.7 ktCO₂. In February, Frontier purchased 47 ktCO₂ of DAC credits from Phlair, and in March, it facilitated 78.7 ktCO₂ (worth roughlyUS$33m) of ERW credits from Eion. Elsewhere, TikTok entered the CDR market for the first time, purchasing 5 ktCO₂ of DAC, Biochar, and Reforestation credits from Climeworks.

Red Trail Energy drives issuance

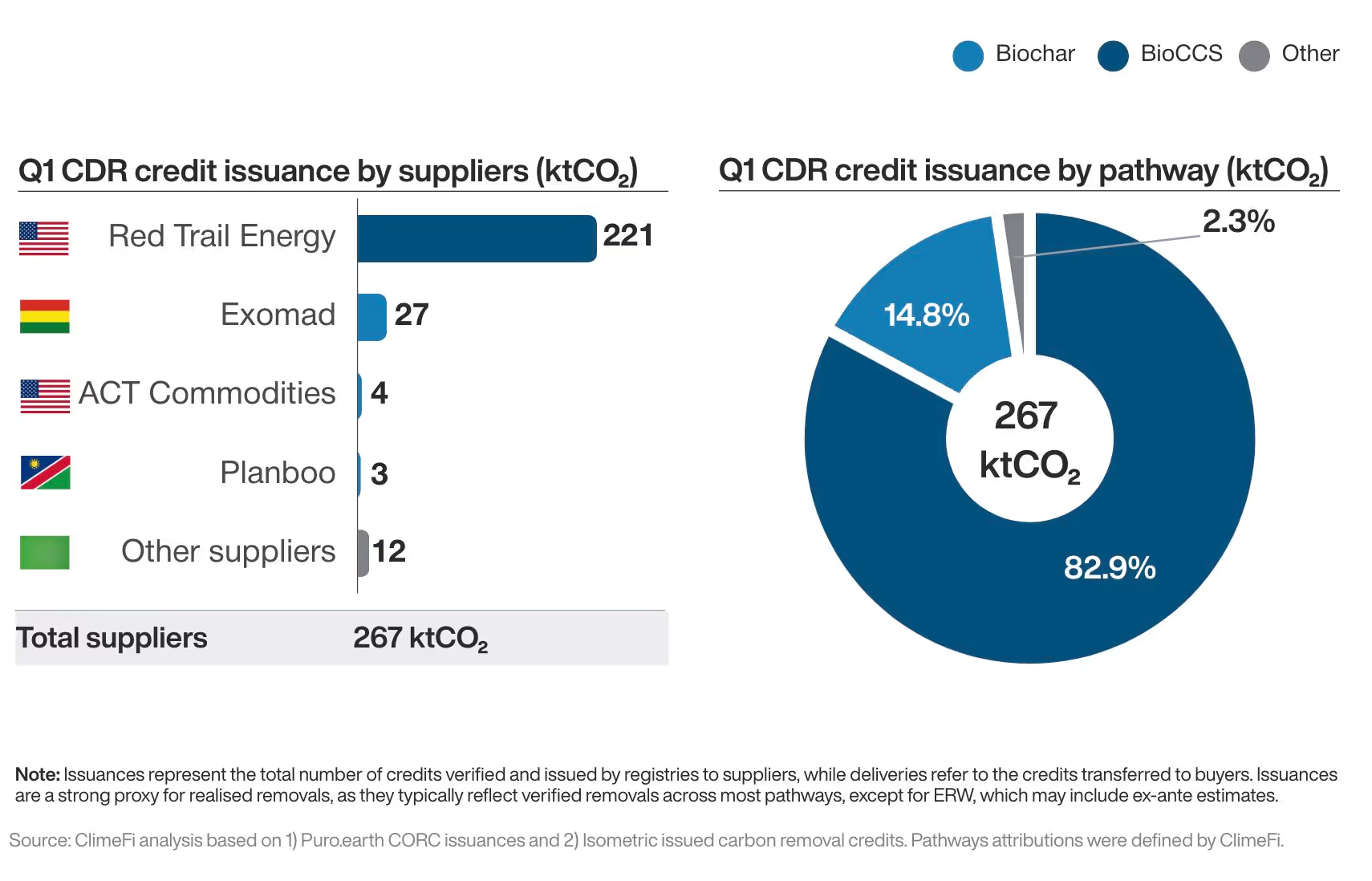

On the supplier side, total credit issuance amounted to 267 ktCO₂. Red Trail Energy – the biggest issuer in FY 2024 – maintained its leading position this quarter, issuing 221 ktCO₂ of BioCCS. It is therefore perhaps unsurprising that BioCCS was the dominant pathway for issuances in Q1, taking 82.9% of the market share.

Funding update: Sweden backs BECCS

A number of important operational project milestones were also met in Q1. Notably, Stockholm Exergi – the Swedish energy provider – announced its final investment decision (FID) to build one of the largest BECCS facilities globally. Once operational in 2028, the new facility – Beccs Stockholm – will have the capacity to remove up to 800ktCO₂ annually.

Helping the project get off the ground, Stockholm Exergi was awarded the Swedish government’s reverse auction for BECCS in January. The approved support amounts to more than 20 billion SEK (around US$1.8bn), most of which will finance the construction and operation of the new facility. Outside of Sweden, Canada is the only other country who has offered public funding support for CDR since the turn of the year, implementing various funding initiatives across DAC and Marine CDR, as well as a new commitment for Canadian-based innovators from the British Colombia Centre for Innovation and Clean Energy (CICE)

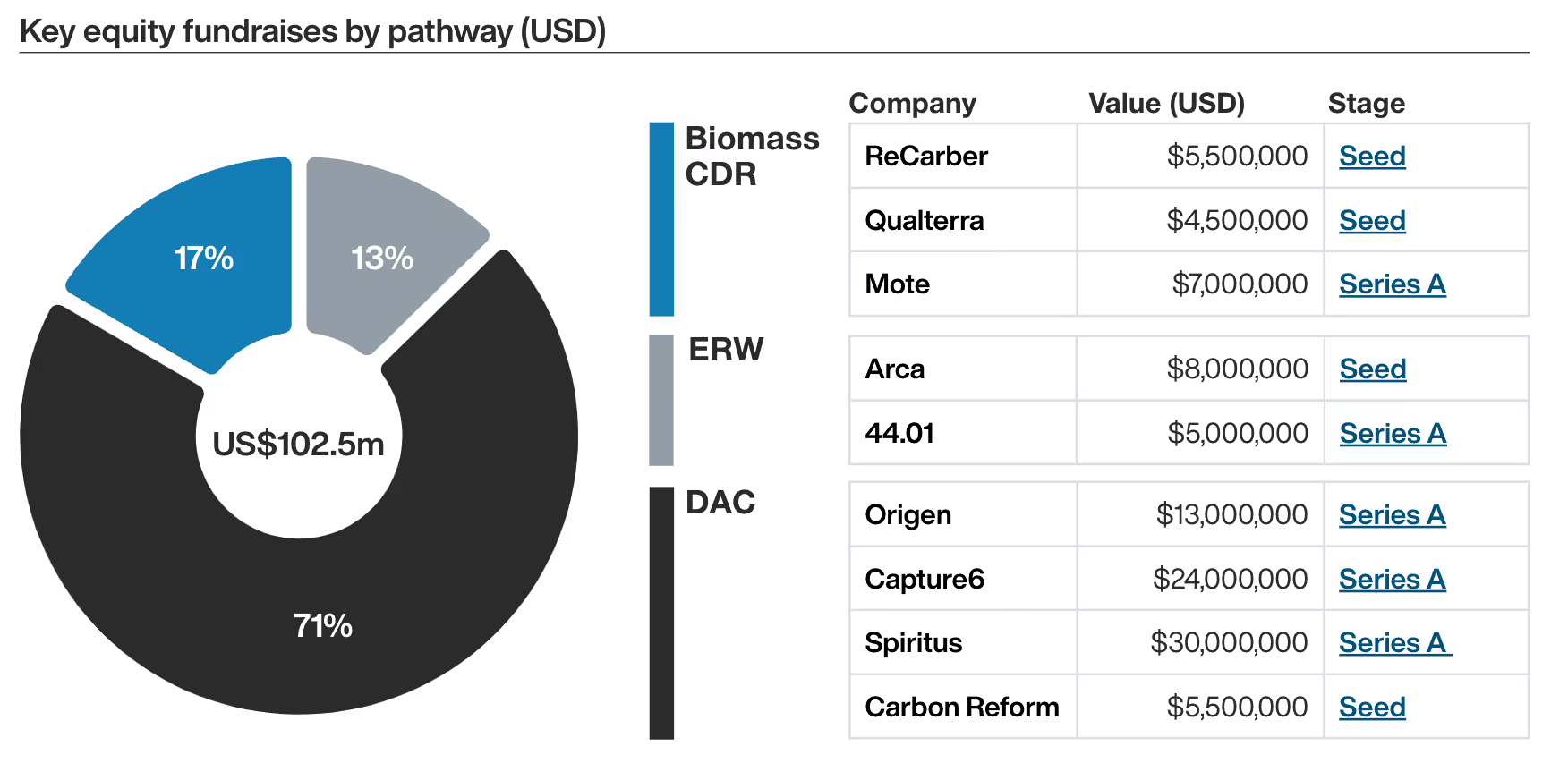

For the third time in five quarters, DAC proved the most popular pathway for private funding, with US$72.5m invested in Q1.