.avif)

A landmark quarter for durable CDR

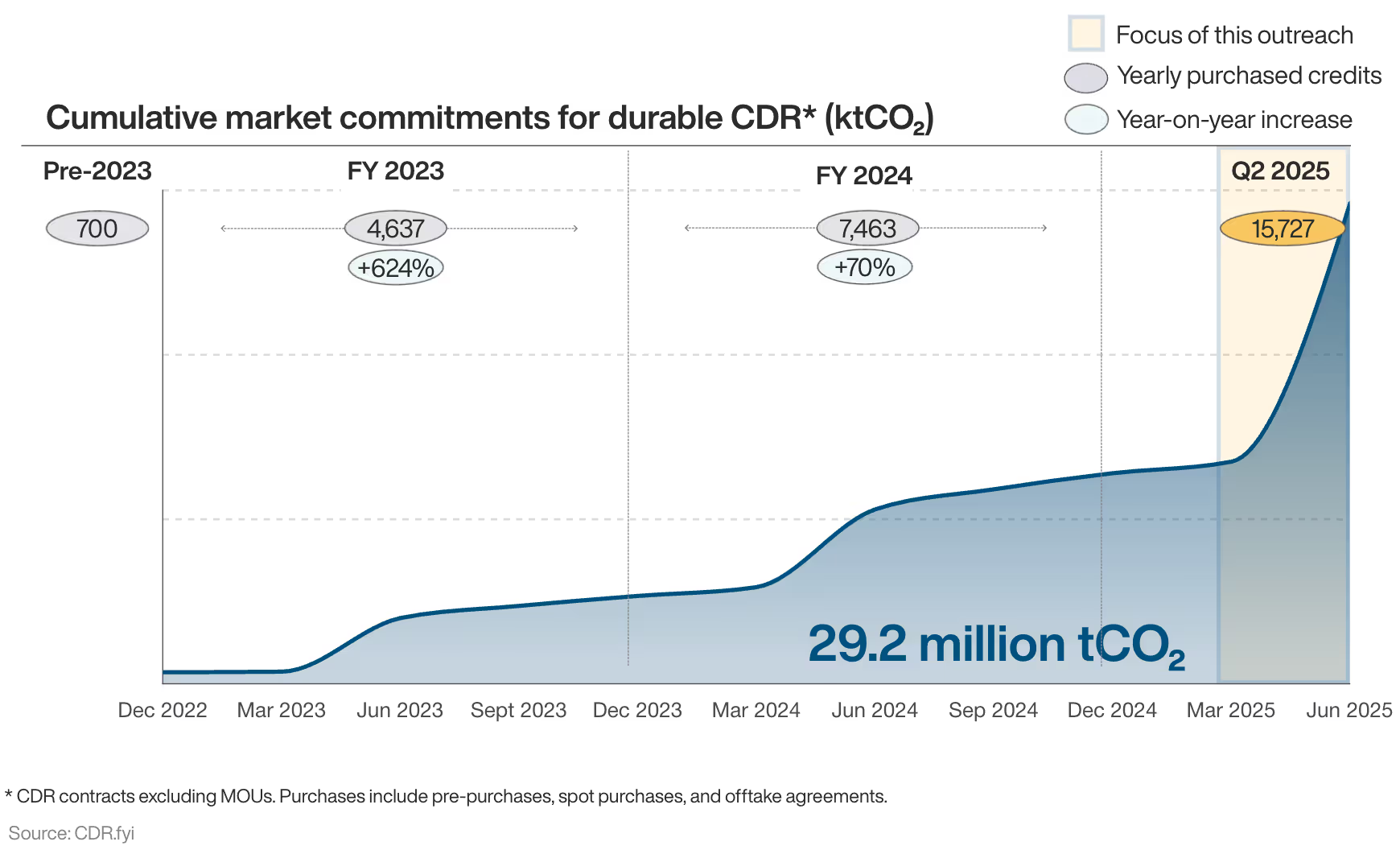

The durable CDR market witnessed an unprecedented surge in Q2 2025, more than doubling in size in the space of just three months. The market jumped from 13.5 million tCO₂ to 29.2 million tCO₂. This growth was fuelled by 15,727 kt of new CDR contracts, representing a 233% year-on-year growth compared to the same period last year.

Remarkably, 2025 has already recorded over twice as many credit purchases than the whole of 2024, with April 2025 recording more purchases than the seven previous quarters combined.

Figure 1

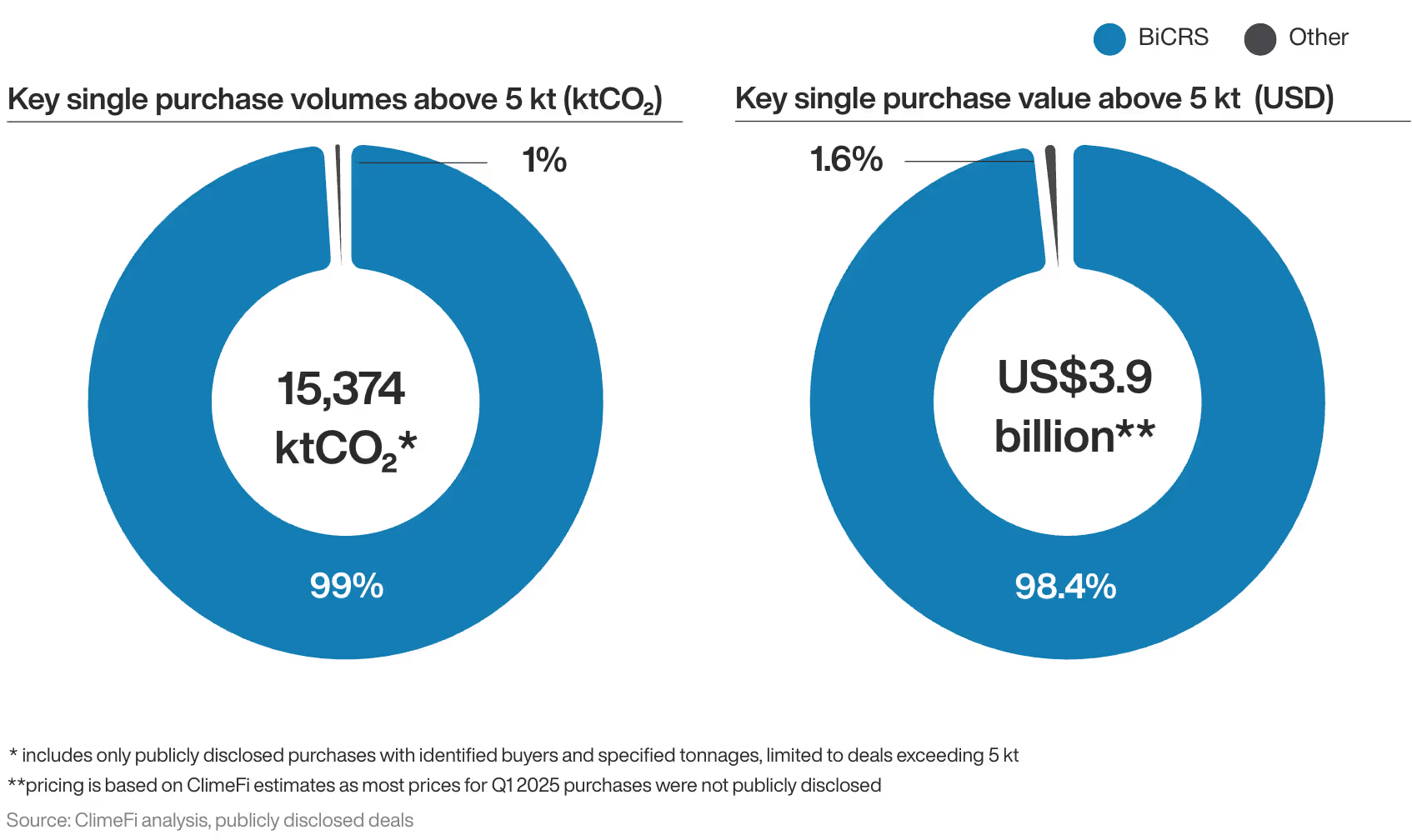

Spending on CDR credits reached an all-time high of US$3.9 billion – a US $2.9 billion increase over the previous quarterly record. Biomass carbon removal and storage (BiCRS) pathways dominated this quarter in terms of purchase volumes, accounting for 99% with all other pathways making up the remaining 1%.

Figure 2

Policy update: EU Green Claims Directive

After weeks of deliberation, the EU is poised to implement its Green Claims Directive – a legislative proposal with significant implications for the CDR market. The directive aims to combat misleading environmental claims, with the EU noting that currently 53% of green claims are vague or misleading and 40% lack supporting evidence.

Crucially, the Green Claims Directive will heavily restrict ‘Carbon Neutral’ or ‘Climate Neutral’ claims based solely on carbon offsetting due to varying methodologies and the potential for double counting emissions. The updated guidance emphasises that companies must prioritise reducing their direct emissions – and then any residual emissions should be addressed with removals. Without removals, most companies will therefore struggle to claim to be carbon neutral.

To substantiate environmental claims, carbon credits must be independently verified and certified, with the Carbon Removal Certification Framework Regulation (CRCF) defining the only Union-issued credits acceptable for compensating residual emissions. This means the CRCF specifies which CDR is valid, and the Green Claims Directive dictates how these certified removals can be used to support environmental claims.

Market update: Norway and Switzerland ITMO transfers

Norway and Switzerland are collaborating on three pilots for cross-border CDR and Carbon Capture and Storage (CCS). Initiatives include:

- Pilot 1: Transfer of a symbolic amount of ITMOs achieved from CDR in Norway (from Inherit Carbon Solutions) under permanent geological storage to a Swiss entity, per Article 6 of the Paris Agreement. This public-private partnership was coordinated by ClimeFi.

- Pilot 2: Transfer of a symbolic amount of ITMOs achieved from CDR in Switzerland from mineralization of biogenic CO2 in recycled concrete to a Norwegian entity, per Article 6 of the Paris Agreement.

- Pilot 3: Transport of CO2 from Switzerland to Norway for permanent storage, if technically feasible and agreed between the commercial partners

This represents the first international Article 6.2 transfers in the durable CDR market. The transaction therefore marks a key milestone in building transparent, rules-based international carbon markets. Norway and Switzerland are cooperating on further pilots for cross-border CDR.’

Major players drive market forward

Q2 2025 saw significant activity from some big names in the CDR space:

- Microsoft set the record for the largest CDR deal this quarter (3.6 million agreement with CO280), only to knock itself off the top spot a few days later (6.75 million tonne agreement with Atmos Clear). Notably, the tech giant also expanded its existing deal with Stockholm Exergi to over 5 million tonnes over 10 years, up from 3.33 million tonnes. In addition, Microsoft’s deal with Exomad represents the largest ever biochar agreement to date.

- J.P. Morgan’s 450 kt purchase agreement positioned the bank as the third-largest CDR buyer, surpassing Google.

- Elsewhere, MOL continued its growing leadership in the space, purchasing CDR for the second consecutive quarter, while TikTok made its second purchase of the year with a 1.75 million tonne agreement in June.

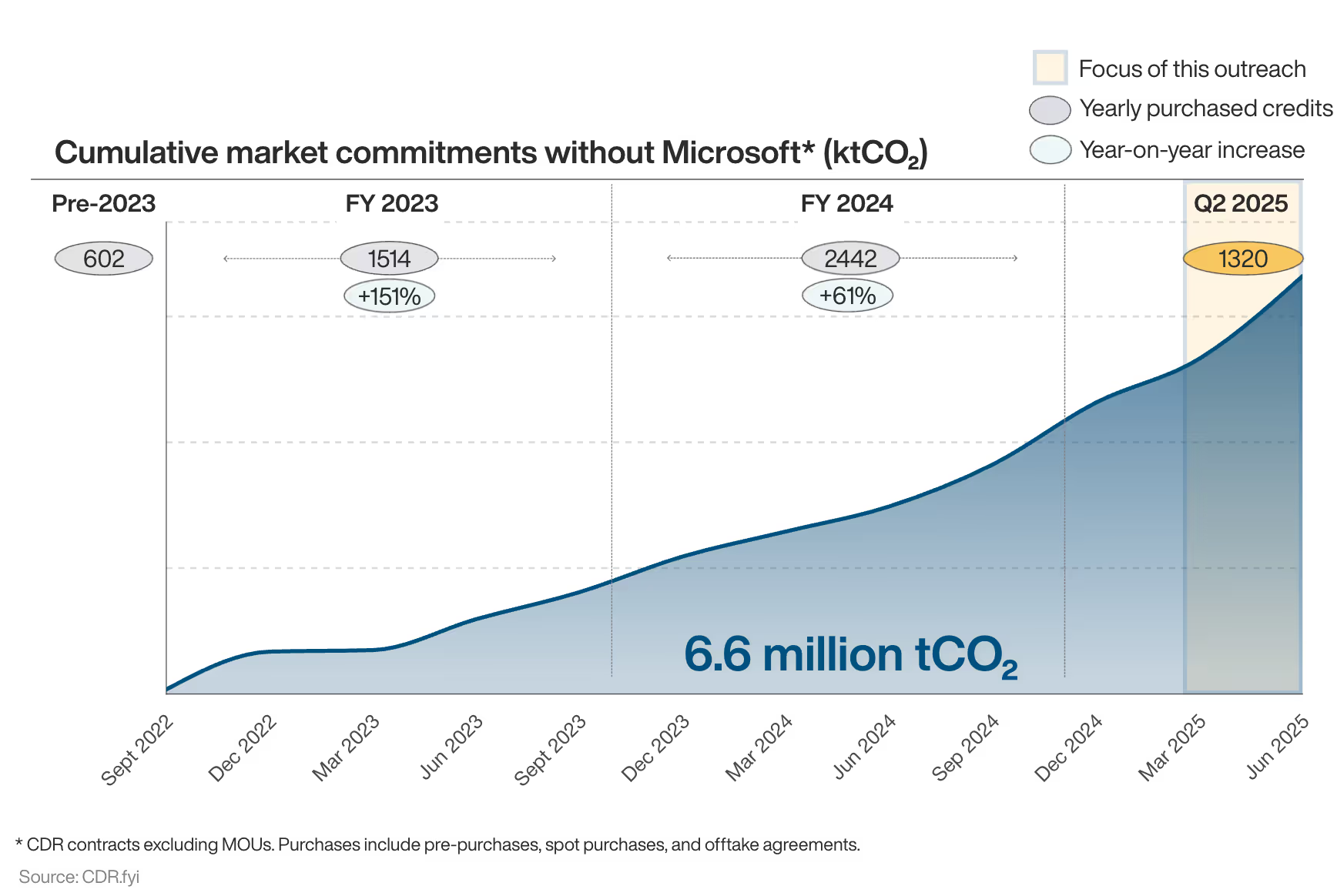

Even excluding Microsoft’s substantial transactions, the CDR market has expanded significantly in H1 this year, with 2,020 kt purchased. Q2 alone saw 1,320 kt of new contracts (without Microsoft), representing a robust 234% year-on-year growth compared to Q2 2024.

Figure 3

Project analysis: credit issuance slows, funding diversifies

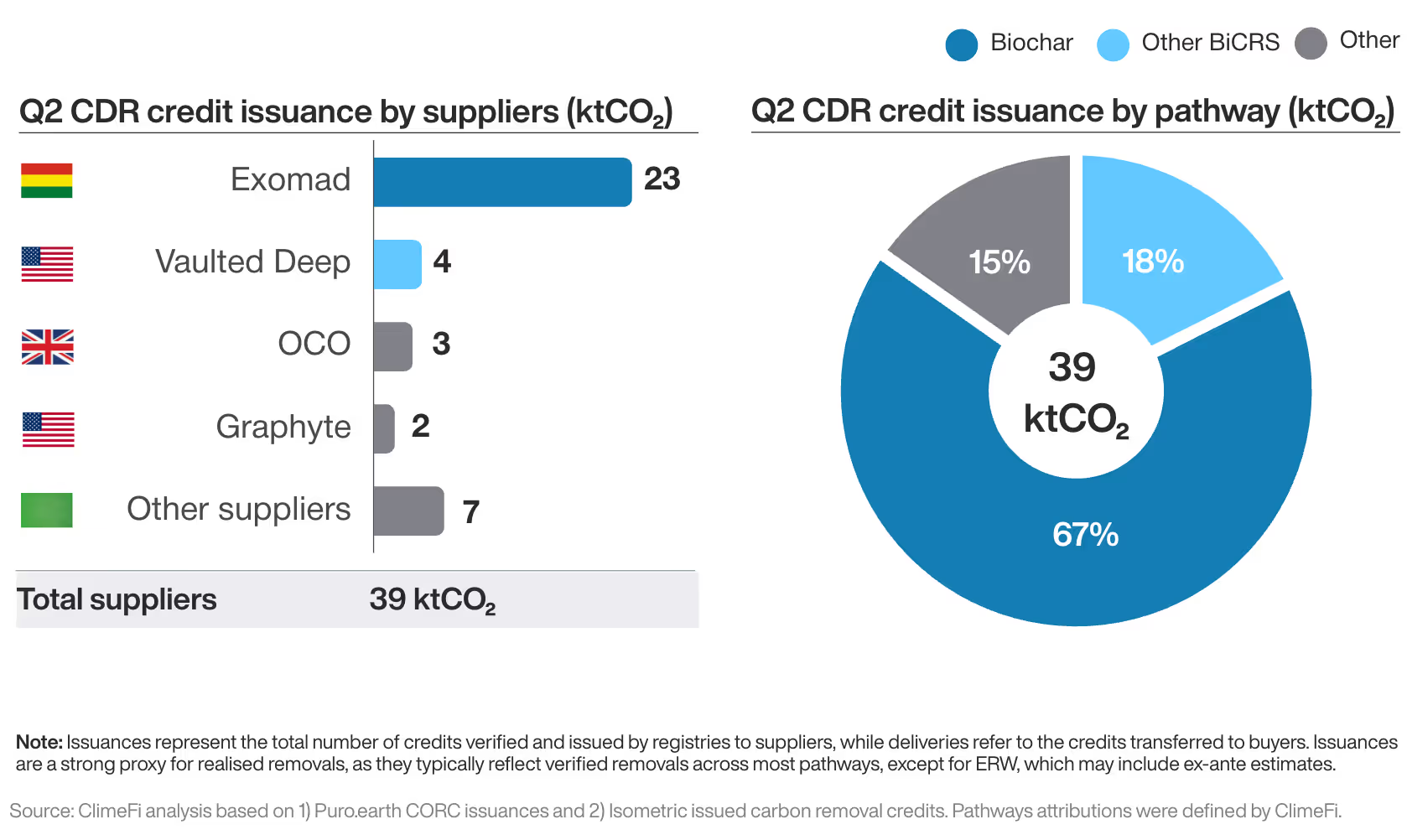

While Q2 was certainly a slower quarter for credit issuance, with an 86% decrease compared to Q1 this year, verified removals across DACCS, Bio-Oil, Marine CDR, and Mineralisation indicate a growing maturity of various pathways.

Notably, 22.5% of credit issuance this quarter came from projects in the U.S., while BiCRS pathways made up approximately 85% of total issuance.

Figure 4

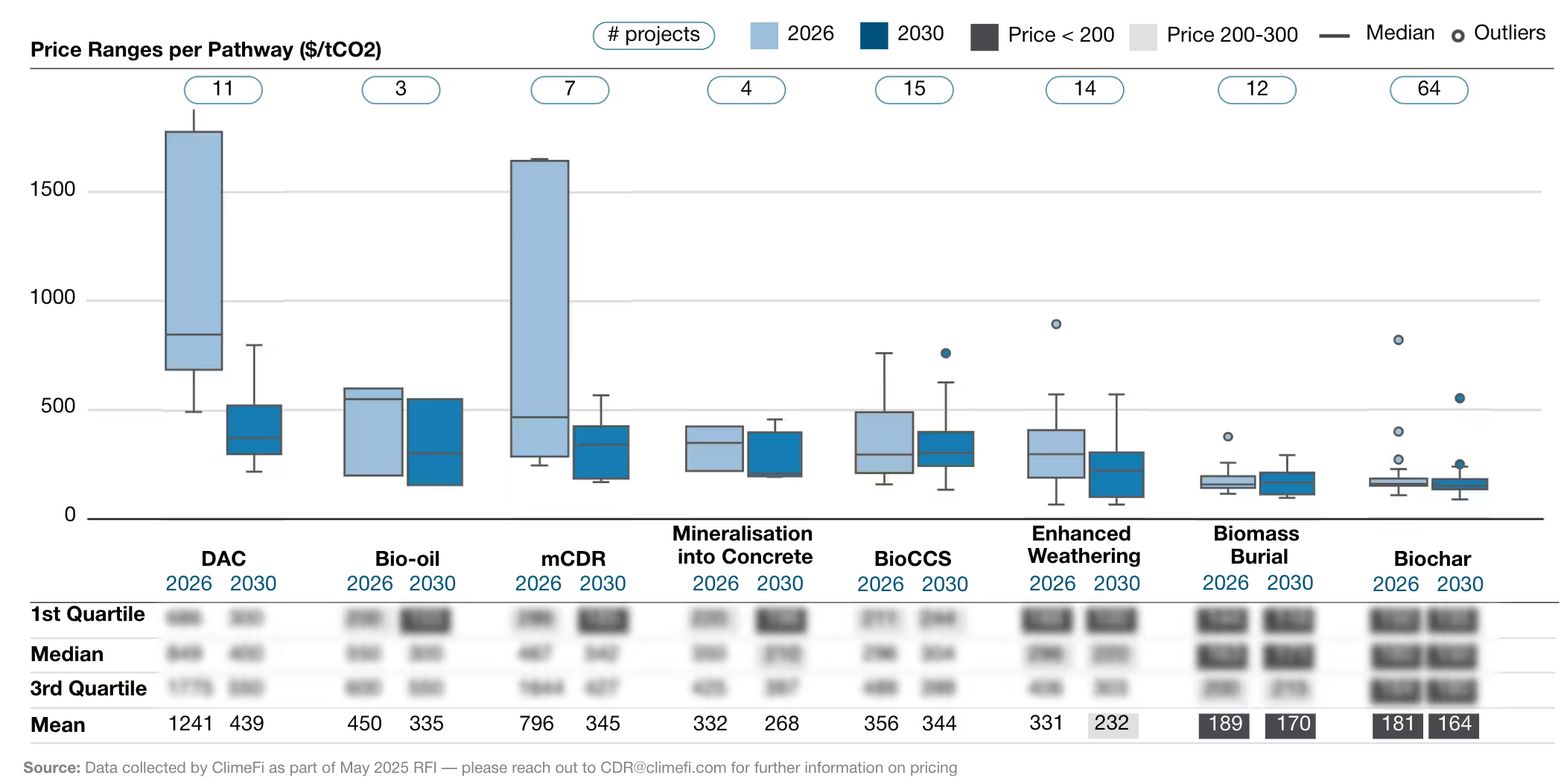

Using data collected as part of a May 2025 RFI, ClimeFi also finds that pricing varies greatly – from 150 $/t for biochar, to 1800 $/t for DAC.

Figure 5

In terms of private funding, Q2 2025 saw US$182 million of combined equity and grant financing, up 78% compared to Q1. Also of note, XPRIZE awarded grants worth US$78 million to the winners of its Carbon Removal competition – US$55 million of which went to EW projects.

Figure 6

In addition to increased equity funding, the emergence of debt financing this quarter perhaps signals a new frontier for the maturing CDR market:

1. ReGenEarth launched a £100 million Green Bond Programme in partnership with circular economy energy experts RER. This initiative will fund the integration of biochar production into existing anaerobic digestion and biomass sites across the UK, employing advanced feedstock and provenance tracking to maximize value in voluntary carbon markets. Investors in this green bond will gain exposure to circular economy projects and voluntary carbon credit markets through secured, asset-backed bonds, with the £100 million bond offering a 12.5% return while financing scalable, carbon-negative biochar solutions.

2. Mati Carbon secured an innovative debt facility from J.P. Morgan, which will be deployed to expand Enhanced Weathering (EW) deployments to new geographies, acquire world-class, high-tech regional laboratory facilities, and develop strategic partnerships to accelerate the global adoption of EW. This innovative financing demonstrates the power of institutional capital to facilitate large-scale durable CDR solutions and serves as a forward-looking example of how developmental climate finance can be deployed to help scale durable CDR while also boosting locally led adaptation.