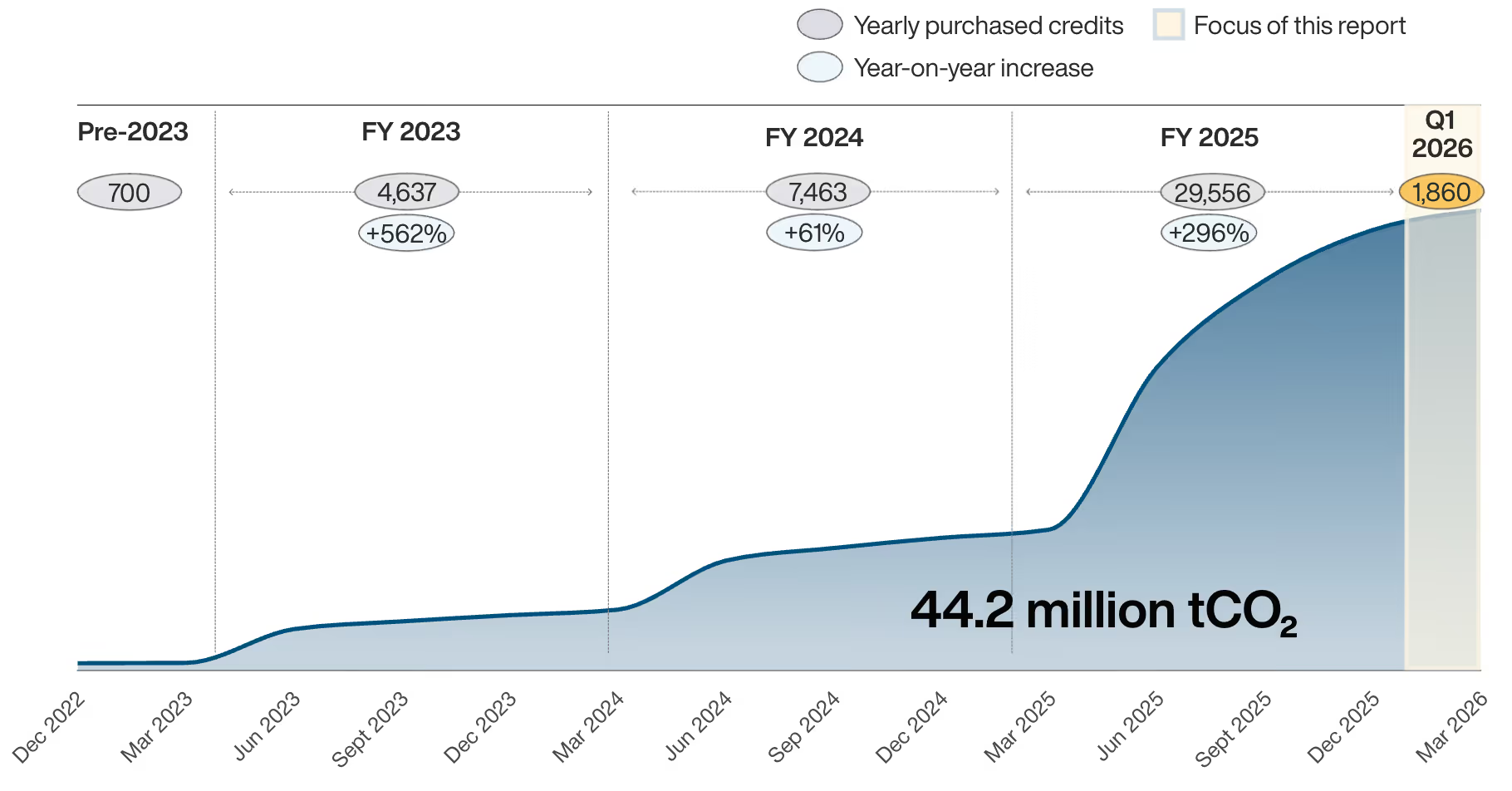

While Q1 is historically the quietest period in the CDR market, 2026 is off to a strong start. 1,860 ktCO₂ of new contracts were signed in Q1 2026 - more than double the 791 ktCO₂ recorded in Q1 2025, and a +135% year-on-year increase.

Figure 1: Cumulative CDR market commitments (ktCO₂)

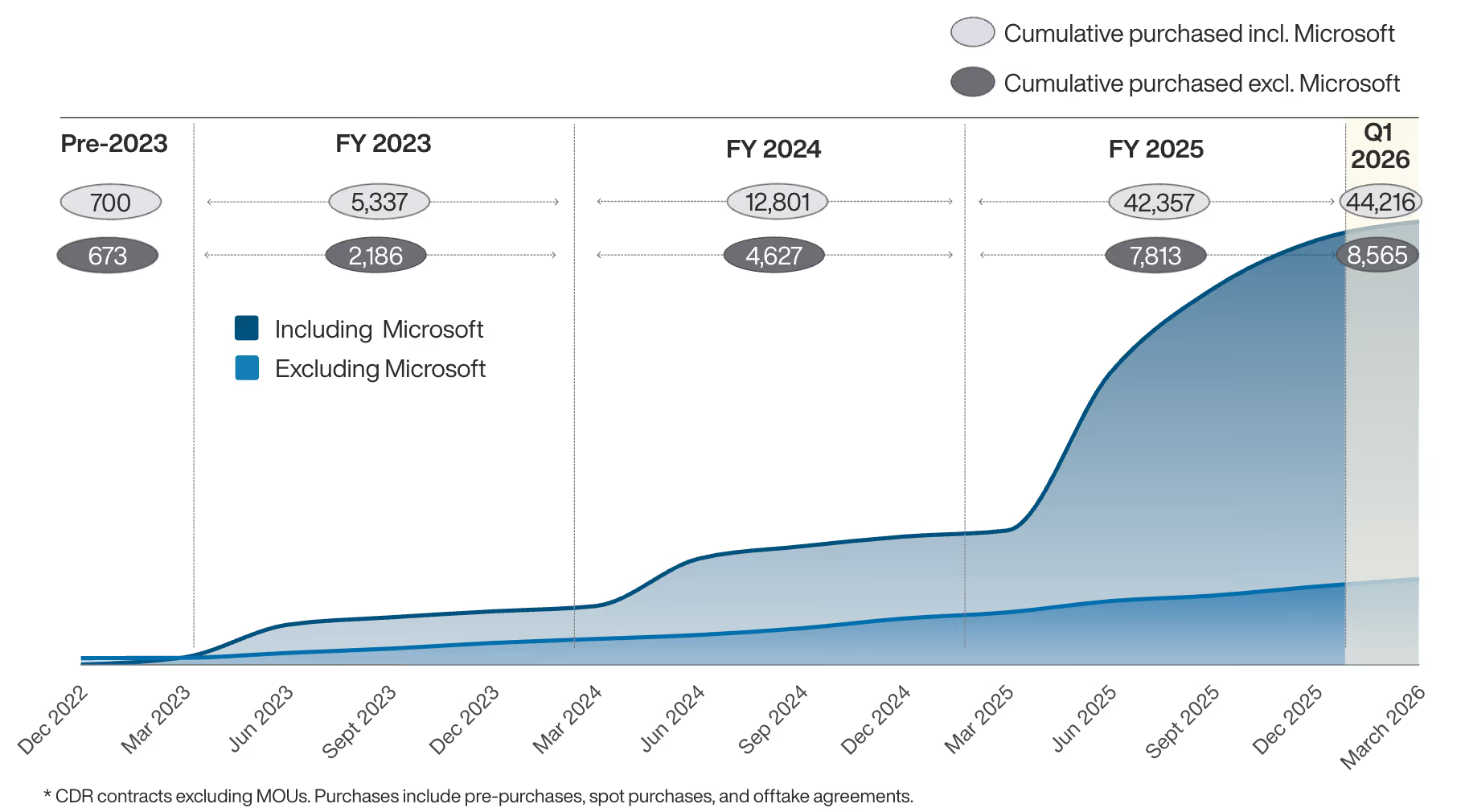

A strong quarter, even without Microsoft

Excluding Microsoft, Q1 2026 still saw 753 ktCO₂ of new commitments - a strong quarter on its own.

Figure 2: Cumulative CDR market commitments without Microsoft* (ktCO₂)

Though Microsoft remains the single largest buyer of durable CDR, and accounts for 81% of all CDR volume to date, non-Microsoft purchases nearly doubled from ~400 ktCO₂ in Q1 2024 to ~750 ktCO₂ in Q1 2026.

This broadening is best demonstrated by the share of non-top-10 buyers that have contributed this quarter. New commitments from buyers such as TD, Salesforce, DNV, and others reached 753 ktCO₂, and non-top-10 buyers contributed roughly 30% of that volume, up from ~17% historically.

However, no new buyers or suppliers entered the market this quarter, suggesting a period of consolidation among existing participants. But those participants are buying more, and the CDR market’s dependence on a few key large buyers is gradually softening.

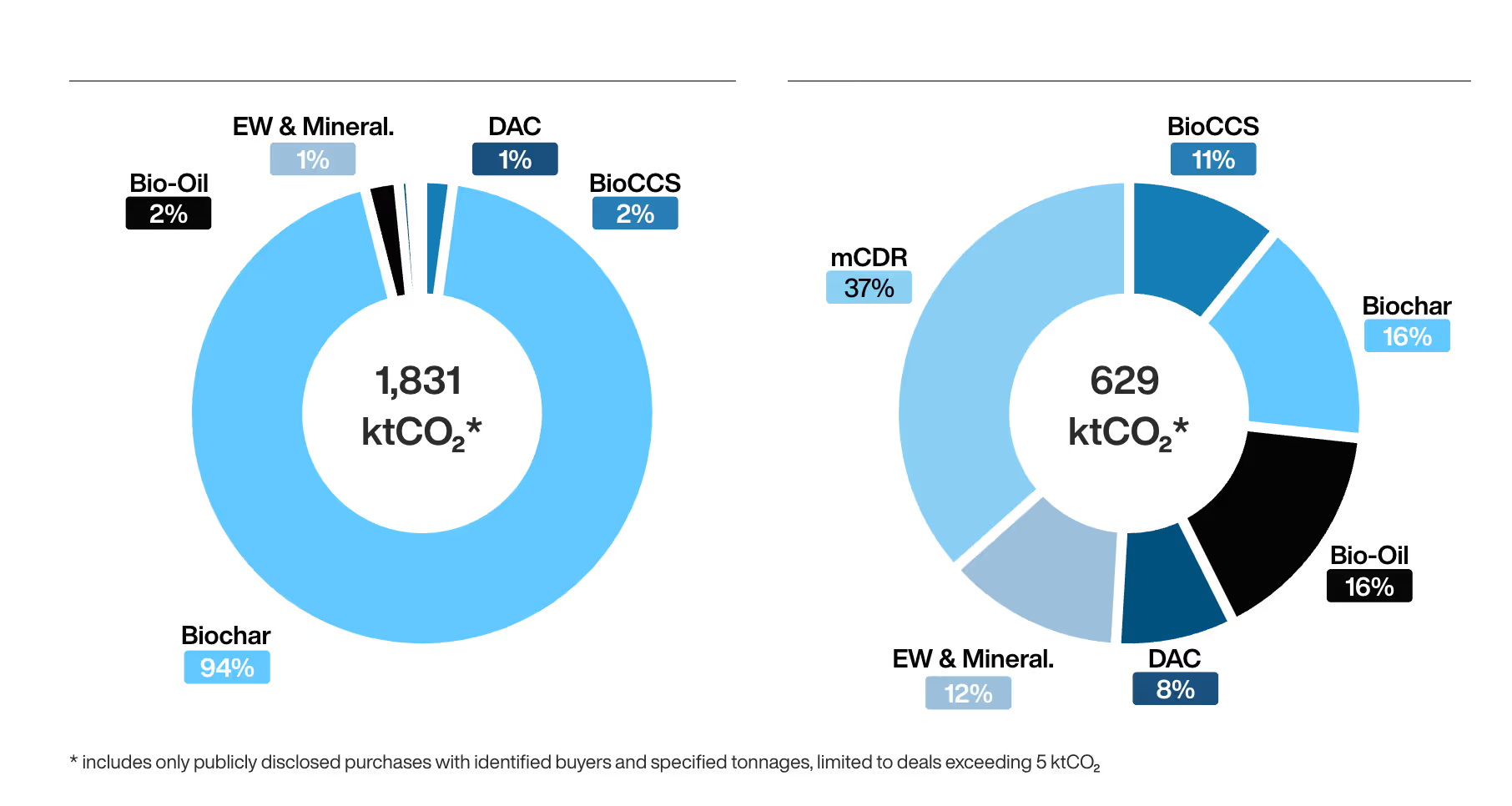

Biochar dominated Q1 2026 purchases, with diversification expected for the rest of the year

Biochar accounted for roughly 94% of Q1 2026 purchase volumes by tonnage, anchored by three large transactions: Liferaft (1 MtCO₂), Empacar (305 ktCO₂), and AMP Clean Energy (200 ktCO₂). It also accounted for 81% of the economic value this quarter, compared with just 7% in Q1 2025.

Early-quarter activity tends to favour proven, near-term supply. Portfolio diversification typically comes later, as new capacity becomes available.

Figure 3: Q1 26 single purchase volumes above 5 ktCO₂ / Q1 25 single purchase volumes above 5ktCO₂*

Regulatory support for durable CDR strengthens

In Q1, the European Commission adopted the first three EU CRCF certification methodologies, while ClimeFi structured the first CRCF transaction.

In parallel, Sweden and Canada led the way when it came to country-level CDR support in Q1 2026.

Investments and funding continue to flow across CDR pathways to support both established and new suppliers

Q1 2026 saw USD 110 million channelled to CDR suppliers across Biochar, BioCCS, EW & Mineralisation, and mCDR.

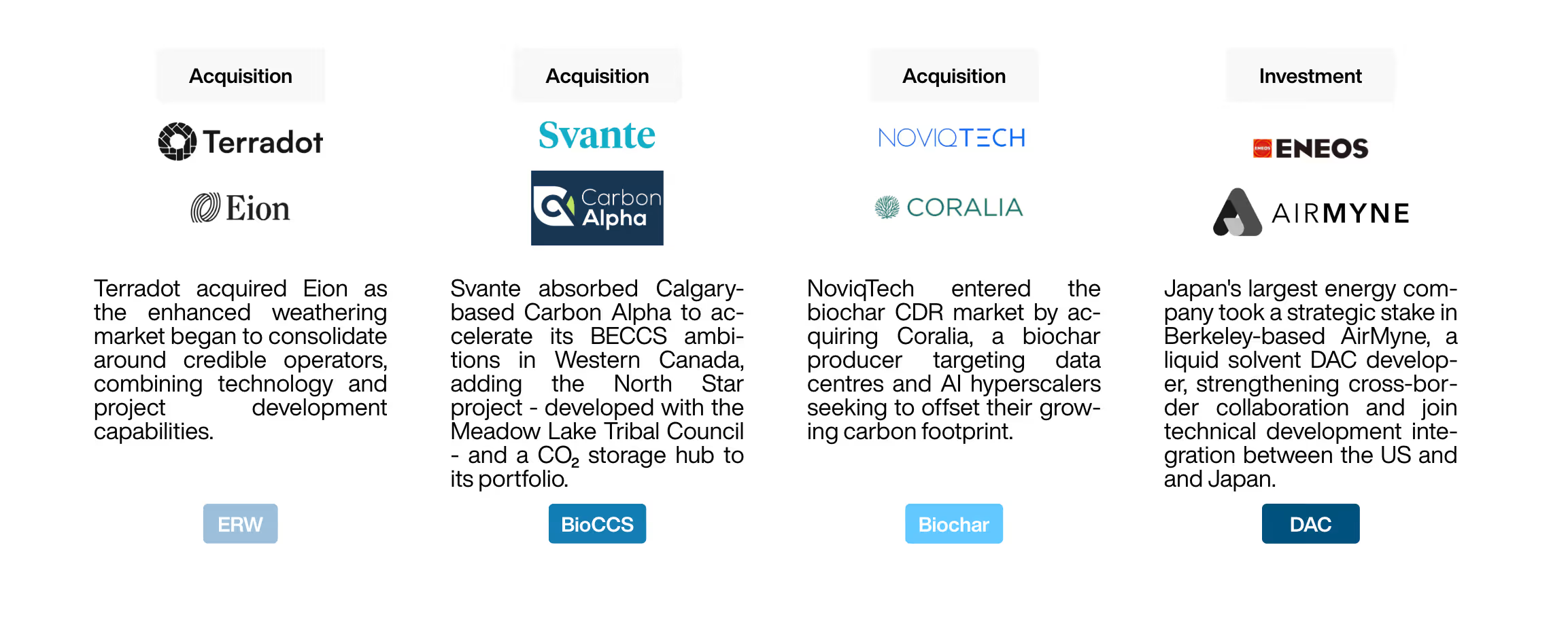

The quarter also saw a wave of mergers and acquisitions.

Behind the analysis

Data for this quarterly review comes from publicly available data, CDR.fyi, and is supplemented by ClimeFi’s own analysis.

For further insights, please download the full Q1 2026 CDR Market Review here